With Alamos Gold’s (TSX: AGI; NYSE: AGI) US$325-million all-share acquisition in July of Argonaut Gold and its Magino mine in northern Ontario, Canada’s third-largest gold producer is on track this year to churn out between 550,000 and 590,000 oz of gold.

The open pit Magino mine, just 300 metres from Alamos Gold’s Island Gold underground mine, and about 83 km northeast of Wawa, will contribute 40,000 to 50,000 oz gold this year, or a 13% increase in the company’s consolidated production and a more than 20% increase in 2025 and 2026.

Next year Alamos expects consolidated production from its three mines in Canada—Island Gold, Magino and Young Davidson—and its Mulatos mine in Mexico, will reach between 575,000 oz and 625,000 oz and climb to between 630,000 and 680,000 oz in 2026.

All-in sustaining costs are forecast to decline from an estimated US$1,250 to US$1,300 per oz this year, down to US$1,175 to $1,275 per oz next year and drop to US$1,100 to $1,200 per oz in 2026.

“The addition of Magino has enhanced our already strong growth profile and its integration with Island Gold is expected to drive significant synergies and open up longer-term opportunities,” CEO John McCluskey says in an interview. “Our costs remain well below the industry average and are expected to decrease significantly over the next several years as we deliver on our low-cost growth initiatives.”

Integration is already going well, McCluskey notes. While the low-grade Magino and high-grade Island Gold deposits are very different, he says, “the ore is virtually identical and allows us to process it all through one common mill.”

'Perfect timing'

About US$375 million of the US$515 million in estimated synergies will come through operational savings from the use of Magino’s 10,000-tonne-per-day mill, approximately 5 km from Island Gold’s headframe, and its large tailings facility. Alamos will save roughly US$140 million in capital costs because it no longer needs to expand the Island Gold mill and tailings facility.

“It would not have been as interesting for us if we had already built a 2,400-tonne-per-day mill but because we hadn’t started that expansion project yet, it was perfect timing,” McCluskey says. “And we were also considering a costly tailings expansion, but we didn’t need to do that either because there was enough capacity at Magino. The cost-savings from those two expansion projects alone was US$140 million, which was pretty meaningful, and the aggregate synergies of over US$500 million exceed the amount of equity we invested.”

Alamos first looked at Magino in 2018 but at that time Argonaut wanted to develop the project themselves. By the time Magino started commercial production in November 2023 the development cost had almost doubled. In 2020 Argonaut estimated the mine would cost $510 million to build, but inflation and other challenges catapulted the final tally to $980 million.

“They were able to do an additional late-stage financing to help them through the completion of the project, but the start-up was not as straightforward as it could have been I guess, and they started running into some financial difficulties” McCluskey says. “That was the beginning of 2024 and at that point it made sense for us to have another discussion.”

In addition to the synergies, McCluskey says there’s optionality to expand mineral reserves and resources at Magino, particularly to the east where Argonaut had run up against the property boundary with Alamos.

There is also the potential to expand Magino’s processing facility.

“Their original intention was to build a bigger mill and run it at a much higher rate — well beyond 20,000 tonnes per day — but capital constraints forced them to pair back their budget and ultimately, they decided to build it in two stages, initially 10,000 tonnes and subsequently increase it to 20,000 tonnes or more," McCluskey says. "They never got there, but they have the permits, so we have that expansion potential to turn it into a more economically attractive mine.”

The CEO notes that by putting the whole district together both projects are stronger and with the greater milling and tailings capacity at Magino, Alamos can potentially increase throughput at its Island Gold mine to up to 3,000 tonnes per day.

“Alamos benefited tremendously but it wasn’t just a one-way ticket. If you unify the camp you can make both projects better and you’ll see a district generating 550,000 ounces a year and doing that for a very long time. That really creates what the industry refers to as a tier-one asset — a long life, low-cost mine located in a safe jurisdiction.”

Alamos has increased global mineral reserves for five consecutive years, and continues to expand in size and quality with potential for further growth. Credit: Alamos Gold

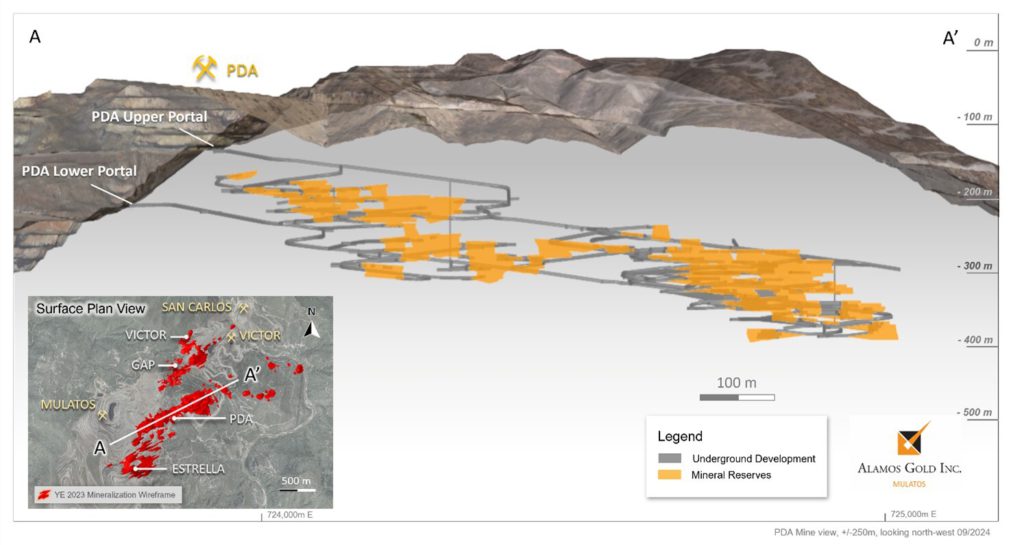

Today about 90% of the company’s net asset value is in Canada. The remaining 10% is in Mexico at its La Yaqui Grande mine located in the Mulatos district, which has enough ore to take it through 2027. However, the company has plans to nearly triple the Mulatos district mine life to 2035 by developing a higher-grade underground deposit adjacent to the main Mulatos open pit called Puerto del Aire (PDA).

In September, Alamos completed an internal economic study estimating a mine life for PDA of eight years producing 127,000 oz. gold annually over the first four years or an average of 104,000 oz a year over the mine life at all-in sustaining costs of US$1,003 per ounce. The study outlined an after-tax net present value (5% discount rate) of US$269 million and a 46% internal rate of return at a gold price of US$1,950 per ounce. Initial capital of US$165 million could be paid back in two years.

Alamos Gold's track record of exploration success at the Mulatos District in Mexico was boosted with the recent news about PDA – a high-return project expected to extend the mine life to at least 2035. Credit: Alamos Gold

The Mulatos mine has been operating for nearly 20 years through the discovery of multiple new deposits in the district. “It’s lasted far longer than anyone has ever imagined,” McCluskey says, “and in the last few years it has had some of its most profitable production.”

“We’ve been exploring for a couple of years now and about three years ago we concentrated on this area called PDA and managed to find structurally controlled high-grade sulphide gold mineralization,” he says. “We drilled it with real impetus behind developing the next project for Mulatos and were successful over the following two years defining about 1 million oz of gold grading at just under 6 grams gold per tonne.”

“That was a great accomplishment and gives us the critical mass we need to take the next step, which is to build a new 2,000 tonne-per-day mill.”

The preceding Joint Venture Article is PROMOTED CONTENT sponsored by Alamos Gold and produced in co-operation with The Northern Miner. Visit: www.alamosgold.com for more information.

Comments