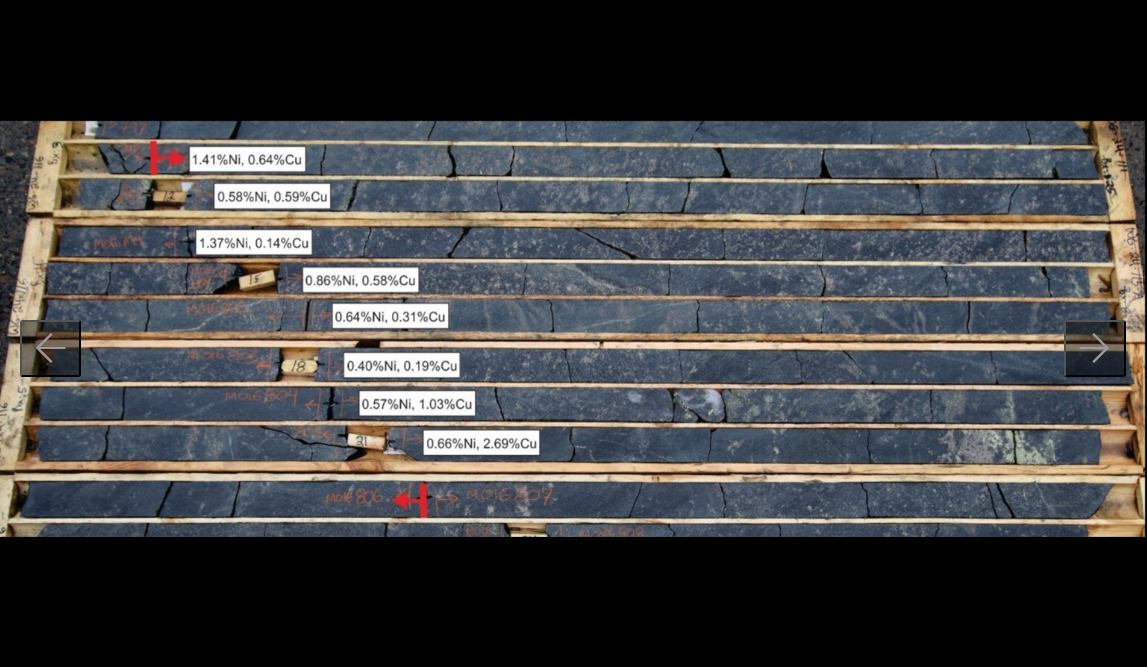

While the prices for key battery minerals such as lithium, cobalt, nickel, rare earth elements, graphite and copper have so far been subdued in 2019, the general excitement about the future wide adoption of electric vehicles continues to fuel activity amongst Canada’s battery mineral juniors. Here is a look at eight such companies.

AVALON ADVANCED MATERIALS

Don Bubar-led, Toronto-based

Avalon Rare Metals is simultaneously developing its Separation Rapids hard rock lithium deposit, 70 km north of Kenora in northwest Ontario, and its Nechalacho rare earth elements project near Great Slave Lake in the Northwest Territories.

The resource at Separation Rapids as of May 2018 stands at 8.4 million measured and indicated tonnes grading 1.41% lithium oxide, with another 1.8 million tonnes at 1.35% Lithium oxide in the inferred category.

Avalon plans to extract up to a 5,000-tonne bulk sample in mid-2019 for trial processing to recover larger quantities of the petalite product for customer evaluation and process flow sheet optimization.

A preliminary economic assessment in August 2018 envisions a plant throughput rate of 475,000 tonnes per year, compared to the 950,000-tonne yearly rate used in a 2016 study. This would result in a 20-year operating life, with annual production of 71,500 tonnes of petalite concentrate; 11,800 tonnes of lepidolite concentrate (both for 18.5 years); and, beginning in year six, 100,000 tonnes of feldspar (through to year 20). The upfront capital expense requirement is $77.7 million, with another $13.7 million planned for a feldspar circuit in years five to six (or once payback of the initial capital is complete).

Average annual revenue is an estimated $90 million versus average annual costs of $60 million, resulting in a pre-tax net present value (NPV), at an 8% discount rate, of $156 million, and a 27.1% pre-tax internal rate of return (IRR). The post-tax NPV is calculated at $102 million and the IRR at 22.7%.

At Nechalacho, in a deal struck in January and confirmed in June 2019, Avalon has attracted private Australian company Cheetah Resources to partner in developing the project’s rare earth resources. Cheetah will acquire ownership of the near-surface resources in the T-zone and Tardiff zones for a total cash consideration of $5 million, while Avalon will keep ownership of the resources in the Basal zone that was the subject of its 2013 feasibility study. Avalon will continue to manage work programs on the property and keep its 3% net smelter return-type royalty.

Avalon is also eyeing small sale re-development of the past producing East Kemptville tin-indium mine in Nova Scotia’s Yarmouth County.

CRUZ COBALT

Vancouver-based junior

Cruz Cobalt describes itself as being “focused on acquiring and developing high grade cobalt projects in politically stable, environmentally responsible and ethical mining jurisdictions, essential for the rapidly growing rechargeable battery and renewable energy sectors.”

Cruz’s Ontario cobalt prospects — Coleman, Johnson, Hector, Bucke and Lorraine — are all located near the town of Cobalt, making the firm one of the largest landholders in this re-emerging cobalt district.

The company’s B.C. prospects include the War Eagle and Purcell prospects, while its U.S. prospects are Chicken Hawk in Montana and Idaho Star in Idaho.

Cruz president and CEO James Nelson has over 12 years of public markets experience focused in finance, investor relations and corporate development in a variety of industries, including energy, mining, oil and gas, and technology, as well as serving as a director and a consultant to several public and private companies.

He has held senior management positions with listed junior companies, including Spearmint Resources and YDreams Global Interactive Tech.

DEFENSE METALS

Vancouver-based

Defense Metals describes itself as being “focused on the acquisition of mineral deposits containing metals and elements commonly used in the electric power market, military, national security and the production of green energy technologies, such as high strength alloys and rare earth magnets.”

Defense Metals has an option to acquire 100% of the 17.8 km

2 Wicheeda rare earth elements (REE) project located 80 km northwest of Prince George in central British Columbia.

It also owns a 100% interest in prospective uranium claims in the northeast section of Saskatchewan’s prolific Athabasca basin. The Geiger project consists of two claims – Geiger North and Geiger South – totalling 12.3 km

2, and is next to the Wollaston-Mudjatik transition zone, described as a “major crustal suture related to most of the major uranium deposits in the eastern Athabasca basin.”

In June, Defense Metals reported that had received successful metallurgical test results for Wicheeda from consulting firm SGS Canada. The junior says results from the first 21 of 25 batch flotation tests completed to date during 2019 showed progressive improvement from early to late stage testing, culminating in test F21 that achieved: 80% recovery of cerium, lanthanum, and neodymium oxides (Ce

2O

3+La

2O

3+Nd

2O

3), 44% rare earth oxide (REO) concentrate grade, and 9.5 times upgrading ratio from head.

FRONTIER LITHIUM

Sudbury, Ont.-based

Frontier Lithium is exploring its Pak lithium deposit in what it calls “Electric Avenue” – a “newly emerging, premium lithium metal district,” hosted in the Canadian Shield of northwestern Ontario.

Frontier describes the deposit as having lithium in a “rare, high purity, low iron spodumene” that is analogous to the Greenbushes deposit in Australia.

The Pak deposit has a measured and indicated resource of 7.5 million tonnes of 2.02% lithium oxide and an inferred resource of 1.8 million tonnes of 2.10% lithium oxide , which has a technical, ceramic grade spodumene with low inherent iron (below 0.1% iron oxide).

The junior recently found a lithium-cesium-tantalum pegmatite showing called Spark, which at surface shows a channel cut with similar grade and composition to Pak. The surface exposure of the discovery is three times larger than the Pak pegmatite, with widths greater than 100 metres, and a strike length exceeding 300 metres.

Frontier’s goal is to “become a low cost, fully integrated lithium producer” by developing Pak, where it has already completed a prefeasibility study to assess the economic viability and technical feasibility of producing lithium concentrates.

In June, Frontier closed an oversubscribed private placement that raised $2 million.

MGX MINERALS

Vancouver-based

MGX Minerals describes itself as a “developer of lithium, magnesium and silicon projects using innovative processes to supply the new energy economy.”

MGX says its “award winning lithium brine extraction technology recovers previously unattainable lithium in produced water from hydraulic fracturing, conventional oil and oil sands (bitumen) production, geothermal brine, and other lithium-rich wastewaters,” and notes that the technology was recognized with a Base and Specialty Metals Industry Leadership Award at the 2018 Platts Global Metals Awards.

Led by chairman Marc Bruner and president and CEO Jared Lazerson, MGX has an intriguing suite of assets that include lithium properties in Alberta and Utah, as well as silicon and magnesium properties in the Rocky Mountains of British Columbia.

MGX operates a 1,000-L/d petro-lithium extraction and water treatment system with partner PurLucid Treatment Solutions, with the system used for large scale testing of bulk water samples from MGX’s petro-lithium projects, including Sturgeon Lake, Alta., and Paradox basin, Utah, as well as customers and partners before deployment of commercial systems.

MGX also says it is “building North America’s next magnesium oxide mine” in the Driftwood Creek mining district, 164 km north of Cranbrook, B.C., where it is carrying out a preliminary economic assessment of an 8.0-million-tonne measured and indicated resource grading 43.31% magnesium oxide.

In June, MGX Minerals spun out of 40% of the common shares of MGX Renewables Inc., with MGX Minerals keeping 18 million shares of MGX Renewables, which will soon list on the Canadian Securities Exchange.

In connection with the spin-out, MGX Minerals took in $2 million in proceeds from a previously completed offering of subscription receipts.

NEO LITHIUM

Neo Lithium is active in South America’s Lithium Triangle at its Tres Quebradas (3Q) lithium brine project, which covers 350 km

2 in Argentina’s Catamarca province.

In May, Neo Lithium filed a reserve estimation within a prefeasibility study that defined proven and probable reserves of 1.29 million tonnes lithium carbonate, with an average grade of 790 mg/L lithium, with a cut-off at 800 mg/L lithium out of a measured and indicated resource of 4 million tonnes, with a cut-off at 400 mg/L lithium.

The study also provided a “mine plan strategy” that would focus on extracting the high grade lithium brine first.

The reserve estimate has a high grade core of 368,000 tonnes of lithium carbonate for the first 10 years, with an average grade of above 1,000 mg/L lithium.

Neo Lithium says this high grade core “is critical, given it enables the company to build less ponds at the beginning of the project, therefore lowering initial capital expenditures, while achieving the target production of 20,000 tonnes of lithium carbonate, as stated in the prefeasibility study.”

The junior notes that this high grade core was only drilled to 100 metres’ depth in the previous drilling campaigns used to estimate the resource and reserve, and that the objective of the 2019 drilling season was to extend at depth the high grade zone in the northern part of the 3Q project.

Neo Lithium also notes it has received geochemical results from 10 samples of the last hole of the season, 1-R-25, that yielded an average over 178 metres (from 87 metres) of 1,117 mg/L lithium. The hole is located on the eastern border of the 3Q lake, an area where the reserve estimation assumed brine to be present to only 10 metres depth; however, the hole found brine all the way from surface to 265 metres’ depth.

It describes the rocks found in the hole as porous halite, sands, silt, clays and gravels from the surface to the bottom of the hole, and notes that drilling stopped at 280 metres’ depth due to technical difficulties.

“We were able to validate this season that our high grade resource and reserve statement have significant potential to increase,” said Neo Lithium president and CEO Waldo Perez. “The 3Q project is today the highest grade project in Argentina, and will continue to grow, as drilling demonstrates the importance of the northern high grade zone.”

NOUVEAU MONDE GRAPHITE

Montreal-based

Nouveau Monde Graphite is developing the Matawinie high purity, flake graphite deposit located 150 km north of Montreal, Que., which Nouveau Monde describes as the “only major North American graphite discovery since 2001.”

Nouveau Monde says its goal is to “become a major low cost producer of anode material for lithium-ion batteries and other value added graphite products with the industry’s lowest environmental footprint, driving sustainable development in the Upper Matawinie region.”

Matawinie, Nouveau Monde says, provides high purity graphite and large flake distribution, plus a location that translates to “strong economics, due to local infrastructure and proximity to customers.”

With the nearby Lac des Îles graphite mine operated by Imerys nearing depletion in 2020, there may be opportunities for Matawinie to step into any supply gap.

Meanwhile, Nouveau Monde is designing a mine at Matawinie that could produce 50,000 t/y of graphite.

According to a March 2017 estimate, Matawinie’s in-pit West zone contains 32.9 million indicated tonnes grading 4.5% graphite, while the South Zone contains 26.3 million indicated tonnes grading 3.73% graphite, plus 19.2 million inferred tonnes of 3.67% graphite.

In recent months, Nouveau Monde has raised $22 million, including $10 million from key shareholder Pallinghurst Graphite Ltd., which gives it secure funding to proceed with construction of a “value added product demonstration plant” at Matawinie.

In May, Nouveau Monde boosted its management team and board of directors with the following appointments: geological engineer Martine Paradis as vice-president and chief engineer for infrastructure and environment; mining engineer Alain Dorval as vice-president and chief engineer for metallurgy and process; co-managing partner of the Pallinghurst Group Arne H. Frandsen as a director; and Christopher Shepherd as a director.

POWER ORE

Toronto-based

Power Ore was spun out in 2018 as an energy metals junior by Stephen Stewart’s Orefinders Resources, and in a transformative move in December 2018, agreed to buy a full interest in the Opemiska copper mine complex from privately held Explorateurs-Innovateurs de Québec.

Power Ore describes the Opemiska copper mine complex as consisting of two past producing underground mines in Springer and Perry, and near the town of Chapais, Que. Falconbridge operated the Opemiska copper mine complex from 1953 to 1991, when it produced a total of 23 million tonnes at 2.4% copper and 0.3 g/t gold.

Since then, Power Ore has pored over data and started drilling at the project, which the junior thinks can be fast tracked, given its jurisdiction, infrastructure, location and a host of other advantages – possibly as a lower grade mine, in contrast to its past as a high grade underground mine.

Stephen Stewart, as Power Ore’s CEO, said in a recent drill results release that “we continue to receive promising results, with this second batch showing widely mineralized copper zones near surface. Mineralization in holes 4 and 6 are once again high grade, near surface holes that clearly shows the open pit potential at Opemiska. Hole 7 is encouraging, as this is an exceptionally wide mineralized zone spanning 130 metres of 0.3% copper, and shows the potential remaining in the crown pillar at Vein No. 3. Most importantly is that we are seeing mineralization very close to the surface, which continues to be in line with our objective of reinterpreting the Opemiska copper complex as an open pit mine.”

This story first appeared on www.NorthernMiner.com.

Comments